Banks engaged in multi-million dollar lobbying effort to protect wealthy tax cheats

Most working Americans cannot underreport their income to the IRS to avoid paying the taxes they owe. Why? Their precise income is reported to the IRS by their employers. You don't hear many people complain about this as an invasion of privacy. It's viewed as a basic step the government takes to collect revenue.

People who don't earn income through wages — business owners and wealthy investors — operate under an entirely different set of rules. In many cases, the IRS receives no information about their income, apart from what the individual voluntarily reports to the government. Moreover, according to researchers, "years of IRS funding cuts, combined with the increased sophistication of tax evasion tactics available to the rich, have made shirking tax obligations easier than ever." In other words, the wealthiest Americans can cheat on their taxes very easily, with little chance of getting caught.

Many rich Americans are taking advantage of this opportunity. The wealthiest 1 percent of American taxpayers are "are hiding more than 20 percent of their earnings" from the IRS annually. According to an estimate by the United States Treasury, "the cost of tax evasion among the top 1 percent of taxpayers exceeds $160 billion a year."

To put that into perspective, the Biden administration proposed $3 trillion in investments over a decade to support families, combat climate change, and improve health care. Senator Joe Manchin (D-WV) says the bill is too expensive and must be cut in half. The savings that Manchin is seeking ($1.5 trillion) is less than the amount that could be recovered if the wealthiest 1% of Americans stopped cheating on their taxes.

The Biden administration is proposing a simple fix to catch wealthy tax cheats. It would require banks to report to the IRS accounts with more than $10,000 annually in deposits and withdrawals. But the banking industry has launched a multi-million dollar lobbying campaign to defeat the proposal.

Banks have attempted to justify this under the guise of protecting "customer privacy." But most of their customers already have their precise income reported to the IRS. Further, under a revised proposal announced this week, there is an "an exemption for wage and salary earners and federal program beneficiaries."

But the bank lobbyists continue to oppose the new reporting requirements. It puts the true purpose of the lobbying effort in stark relief: protecting the banks' wealthiest customers from tax enforcement.

How does Biden’s bank reporting proposal work?

According to the proposal, banks will be required to collect and report two new data points to the IRS: the total amount deposited and withdrawn annually from bank accounts with at least $10,000 in transactions.

This amount will not include income from W-2 wages or federal programs, such as Social Security. The aim of this proposal is to equip the IRS to identify discrepancies between what high-income taxpayers report and what they actually have in the bank. Further, banks will be able to report these totals to the nearest $1,000. Taxpayers making under $400,000 will not be subject to more audits, according to the Biden administration.

Yet, in an effort to derail the proposal, many opponents are grossly micharaterizing the new reporting requirement. Specifically, critics are suggesting that the IRS will have access to information that will allow them to track individual transactions.

On September 9, right-wing pundit Candace Owens tweeted, “The Biden administration is attempting to empower the IRS to monitor every single withdrawal, deposit, and transaction you make from your personal banking accounts, PayPal, Venmo, etc.”

Lawmakers are also contributing to this misinformation. Earlier this month, Senator John Barasso (R-WY) said on Fox News that the proposal will give the IRS the authority to “rifle through your checking account, to look at any check that you either deposit or write for over $600.” House Minority Leader Kevin McCarthy (R-CA) said in a press conference on September 30 the proposal will allow the IRS to “spy on anything you buy that costs $600 or more.” On October 5, Senator Mitch McConnell (R-KY) wrote in an op-ed that the proposal “give the IRS sweeping new authority to snoop on Americans’ personal finances.”

These claims are all false. Administration officials have emphasized publicly several times that banks will only be reporting “the most basic, high level information on account inflows and outflows.”

“Imagine a taxpayer who reports $10,000 of income; but has $10 million of flows in and out of their bank account. Having this summary information will help flag for the IRS when high-income people under-report their income (and under-pay their tax obligations),” the Treasury Department wrote in a Fact Sheet on the proposal.

Other critiques include that these new reporting guidelines will be costly to implement. Yet, according to the administration, taxpayers won’t have to do anything. Further, experts believe this will be a “minor change” for banks and “virtually cost-free.” Financial institutions are already required to report information to the IRS on bank accounts with more than $10 in interest income.

“We’re simply asking to add two boxes to that IRS form, one that would be the aggregate inflows into the account over the course of the year, and the second would be the aggregate outflows from the accounts. So it’s not detailed information,” Treasury Secretary Janet Yellen explained.

Banks launch massive lobbying campaign against IRS reporting

For months, banks have been spending millions of dollars to lobby against the new IRS reporting requirement.

Between April and June of this year, the Independent Community Bankers of America (ICBA), a trade group for small banks, spent $830,000 lobbying the House, Senate, and Treasury Department, including on “Bank Account Information Reporting to the IRS,” according to lobbying disclosures. Then, from July to September, it spent $940,000 on lobbying, including efforts to bar new IRS reporting.

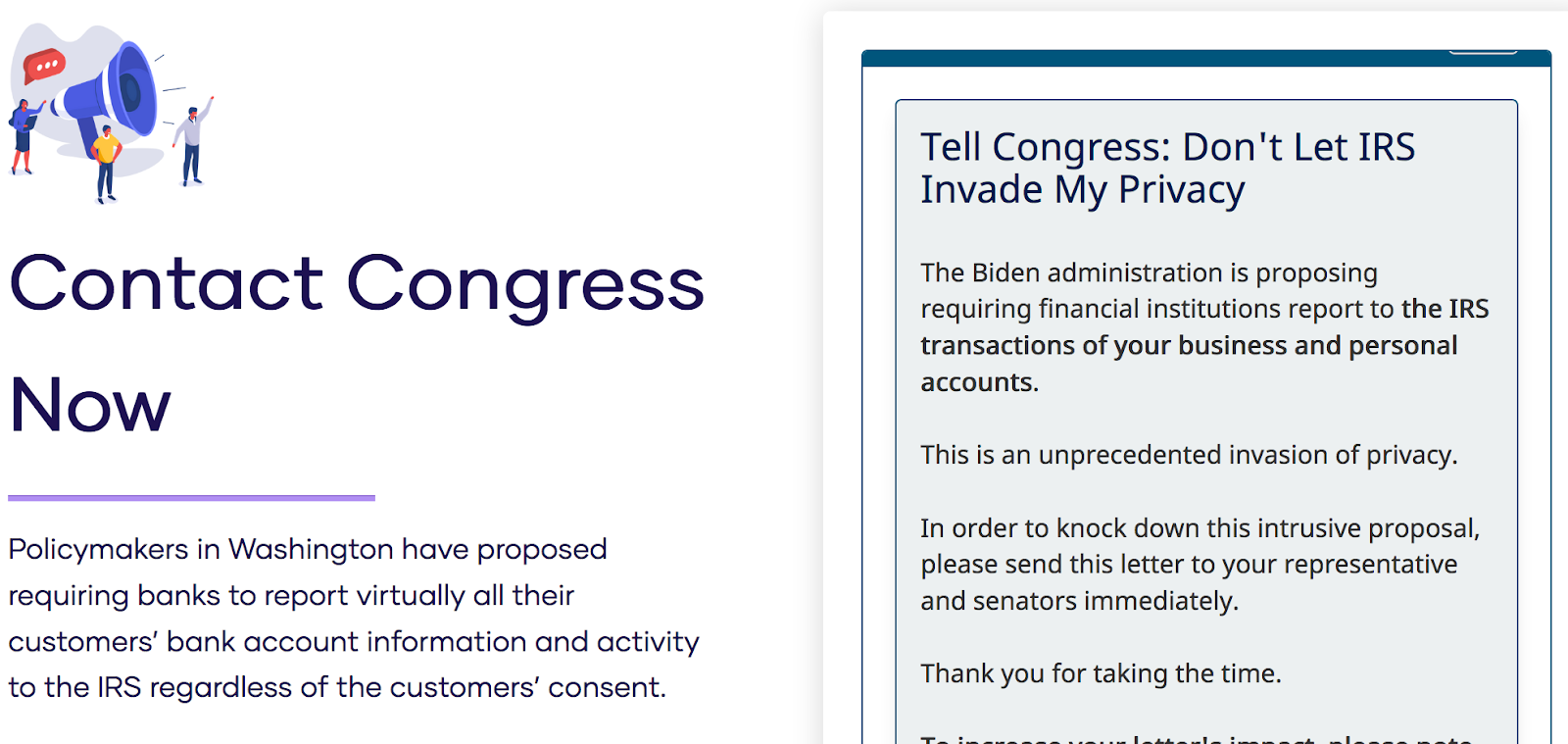

On its website, the ICBA falsely claims that the proposal will force banks “to report virtually all their customers’ bank account information and activity to the IRS regardless of the customers’ consent.” It urges site visitors to “Contact Congress Now” and “Tell Congress: Don’t Let IRS Invade My Privacy.”

Elsewhere, the ICBA asserts that “the Proposal would require financial institutions to perform a police function on behalf of the IRS.” A few months ago, the organization also conducted a survey with Morning Consult where it found that “67% oppose a proposal that would allow the IRS to collect bank account deposit and withdrawal information from American consumers.” The survey does not clarify that the IRS would collect aggregate information on an annual basis.

Meanwhile, the American Bankers Association (ABA), a group that represents big banks, has spent $2.6 million over the last three months lobbying the House, Senate, and Treasury Department on a variety of issues, including Biden's plan and the “Tax Gap Reform and IRS Enforcement Act”–– a bill introduced by Republicans to thwart IRS data collection from banks. In the previous quarter, ABA spent $2.5 million lobbying.

In September, ABA sent a letter to the Senate Finance and House Ways and Means Committee saying that the Biden administration proposal would impose a “significant burden on small businesses and community banks and add no discernible value to tax enforcement.”

Most recently, on October 19, ABA President Rob Nichols issued the following statement:

The exclusion of payroll and federal program beneficiaries does not address millions of other taxpayers who would be impacted by the proposal. Not every non-wage worker is a millionaire. How about self-employed hair stylists, convenience store owners and farmers just to name a few?

Yet, as the Treasury Department and administration officials have explained, the enforcement proposal would not target all non-wage workers. Rather, it would zero-in on the wealthy. Self-employed hair stylists or convenience store owners would not be impacted –– unless, of course, they’re millionaires evading taxes.

This issue should spark outrage across the political spectrum and yet I imagine there will be very little said about what the banking lobby is doing here. American politics is in a dreadful state right now.

Thank you for posting about this. My sister ran a great little company, employed 10 people, and was able to just scratch out about $50k/year for her salary. During the 10 years she ran the company, she was audited by the IRS THREE TIMES, each audit taking 4-6 months. The first one found nothing wrong. The second one found out she'd overpaid and they gave her a small refund. The third audit showed she'd overpaid, but by a smaller amount than previously. All of this time and effort by the IRS came to exactly ZERO results, caused undue stress and down time for my sister's business, and eventually she closed the company to avoid further business-decimating intrusions by the IRS. Meanwhile, the rich were getting off with obvious and apparent tax evasion tactics, and well-known techniques. Shine more light on the failure of the IRS to do its basic duty of collecting taxes, please! This needs to change NOW.