Buying the competition

Over the last year, prices for groceries are up 13%. Meanwhile, the price of food at restaurants has increased more slowly at 8.5%. Why? Restaurants are a highly-competitive industry. The grocery industry, on the other hand, has been consolidating. The total number of grocery stores in the United States "declined by roughly 30% between 1994 and 2019."

Higher prices have fueled record profits for Kroger, the nation's largest grocery store chain. Kroger recorded a $3.5 billion profit in 2021 and projects an even larger haul, $4.9 billion, in 2022. Kroger itself has fueled the consolidation, acquiring a slew of competing chains, including Harris Teeter and Fred Meyer. Kroger, which operates 2700 stores under a variety of brand names, has been able to pass on large price increases without losing businesses to competitors.

Now, Kroger wants to get much bigger.

Kroger recently announced an agreement to purchase Albertsons, the nation's second-largest grocery store chain, for about $25 billion. Albertsons itself acquired another major competitor, Safeway, in 2015 for $9.2 billion. The Kroger-Albertsons deal, which is subject to review by the Federal Trade Commission (FTC), would create a grocery behemoth that would "operate nearly 5,000 stores across 48 states and the District of Columbia." The combined entity, with revenue exceeding $200 billion, would control about 22% of the grocery market in the United States, trailing only Walmart.

The impact on competition would be even more pronounced in certain markets, particularly on the West Coast, where Kroger and Albertsons both have a large number of stores. Across the country, "48% of Albertsons’ stores were located within three miles of a Kroger location." According to Stacy Mitchell, co-executive director of the Institute for Local Self-Reliance, a combined Kroger-Albertsons and Walmart "would control 70 percent or more of the [grocery] market in 167 cities in the United States."

Kroger claims the merger would benefit consumers, pledging to "invest $500 million to lower prices" over four years as part of the transaction. While that sounds significant, it's a drop in the bucket for a combined entity that expects to have more than $200 billion in revenue. If Kroger would have provided $125 million in price reductions last year, it would have reduced its profit margin from 22.7% to 22.6%.

Further, it's unclear how anyone could independently verify whether Kroger provides the modest discounts it is promising. Kroger says it "has not determined specifics" because "the companies cannot share certain information as long as they are separate."

Historically, grocery store mergers have resulted in reduced competition and higher prices. An influential 2008 study "found that in four of the five mergers they evaluated, [grocery] prices appeared to have increased between 3 and 7 percent."

A spin-off destined to fail

Section 7 of the Clayton Antitrust Act, enforced by the FTC, prohibits acquisitions that substantially "lessen competition" in "any line of commerce." Even Kroger acknowledges that the proposed acquisition of Albertsons would lessen competition in many markets. But Kroger has a plan to secure approval of the merger by the FTC anyway.

Kroger is proposing divesting Albertsons of "between 100 and 375" prior to the merger. These stores would be spun off into a separate company. The concept is that this new company would preserve competition in areas that would otherwise be dominated by a combined Kroger/Albertsons.

Divestiture is a popular tactic to secure approval for large acquisitions. To secure approval of its acquisition of Safeway, Albertsons agreed to divest 168 stores. Those stores were purchased by Haggen, a much small competitor, for $1.4 billion. But the stores that are divested are seldom top performers. Haggen was unable to successfully operate the locations and, a few months after acquiring the stores, declared bankruptcy. Ultimately, it sold 29 of the stores back to Albertsons. Others were closed entirely.

Notably, Kroger is proposing to spin off the divested Albertsons stores in case it’s unable to sell the stores to a competitor. That's because there are so few major competitors remaining. It's unlikely any of them will be interested in acquiring a small collection of Albertsons' least profitable stores and competing head-to-head with Kroger.

The looting of Albertsons

Kroger's acquisition of Albertsons may or may not be successful. But Apollo Capital Management and Cerberus Capital Management, the private equity firms that own 75% of Albertsons, aren't waiting around for their payoff. Instead, they have the scheme to cash out now.

Along with the merger, Albertsons announced a plan for a "special dividend" of $4 billion. The dividend represents about one-third of the total market capitalization of Albertsons. The dividend will not come from "surplus profits, but rather out of critical operating margins it needs to stay afloat over the next twelve months." Albertsons will use $2.5 billion of cash on hand and finance the remaining $1.5 billion through loans. The special dividend would reduce Albertsons' available cash on hand by 75%. And Albertson's already has $6.55 billion in existing debt.

Albertsons originally planned to issue the dividend on November 7. But it is on hold until at least December 9 after Washington State Attorney General Robert Ferguson challenged it in court. Furgeson argued that the dividend would "cripple Albertsons’ ability to operate its stores and meaningfully compete with Kroger during the time before the deal closes and leave it in a weakened state if the deal subsequently falls apart." If the $4 billion dividend is paid out, Furgeson says, Albertsons "will be in the position of arguing to federal and state antitrust enforcers that it is preferable to allow Kroger to purchase its remaining assets because it is a failing firm."

Prices at Albertsons are already quite high as a result of financial engineering imposed by its current owners. Albertsons, for example, sold some of its real estate to fund dividend payments, and now has billions in rent obligations.

How Kroger treats workers

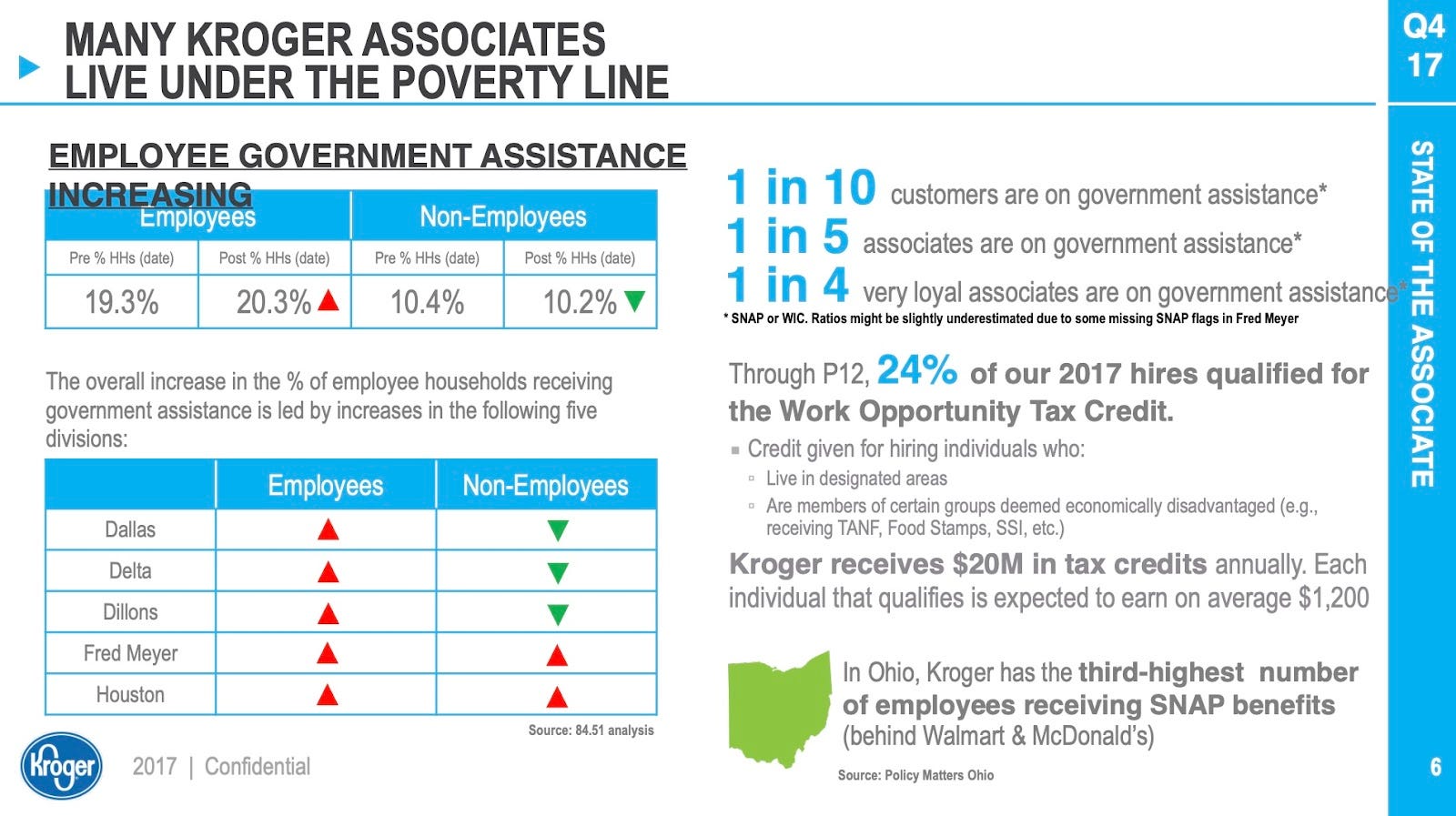

A report published by the Economic Roundtable documents the economic struggles of Kroger employees. The report surveyed 10,287 Kroger workers in the Puget Sound region of Washington, Colorado, and Southern California. It is the "largest independent survey of retail workers that has ever been conducted in the United States." The survey was unwritten by the the UFCW, the union which represents many Kroger workers.

Kroger is the sole employer for 86% of its workforce, and workers earn an average wage of $29,655. This is not a living wage nearly everywhere that Kroger operates. Two-thirds of Kroger workers "say they do not earn enough money to pay for basic expenses," like rent and groceries, on a monthly basis. 14% of Kroger workers say they are currently homeless or have been homeless in the past year. Another 36% worried about being evicted from their homes.

The Economic Roundtable report found, while Kroger workers are surrounded by food, "over three-quarters of Kroger workers are food insecure," which means they "cannot afford balanced and healthy food." These workers "run out of food before the end of the month, skip meals, and are hungry sometimes." (Kroger workers receive just a 10% discount "on Kroger brand groceries, which excludes fresh produce.")

A confidential 2018 Kroger report, obtained by More Perfect Union, acknowledged that "hundreds of thousands of employees live in poverty and rely on food stamps and other public aid as a result of the company’s low pay."

If Kroger's purchase of Albertsons is approved, the combined company will employ more than 710,000 people. Kroger has closed stores rather than abide by local ordinances and pay a few more dollars an hour to its workers. The reduced competition in the grocery industry could "increase Kroger’s ability to set wages beneath what a competitive market would deliver."

Well first, thank you for this exhaustive investigation. I hope the current administration will continue to challenge this monopolistic activity. This is one of those areas of our economy that needs comprehensive and modern legislation backed by well funded agencies and knowledgeable staff. I think that most of the political awareness of us all is spent on the current nonsense. Yes the current nonsense is serious but it takes all the oxygen out of the room. For the media it is just not “sexy”. I despair, but please keep unearthing these less sexy stories that are nevertheless of profound impact.

This merger should not be allowed. It really doesn't get more complicated than that.