One company’s million-dollar gambit to turn the healthcare crisis into a gold mine

Today, Americans are facing dramatically increased health care costs, with millions losing coverage and one in three cutting back on daily living expenses to cover medical bills.

For the health savings account (HSA) industry, however, these are boom times. In a triumphant March 17 earnings call, HealthEquity, the nation’s largest administrator of HSAs, reported “accelerating earnings power… significant margin expansion, and record HSA sales.”

Stephen Neeleman, HealthEquity’s founder and board vice chairman, attributed the company’s recent success to policy changes enacted by the Trump administration. During the call, Neeleman credited Trump’s “One Big Beautiful Bill” for expanding HSA eligibility. He called the new law “the most significant structural change to the HSA market since the accounts were created.”

HSAs allow people to set aside a portion of their pre-tax income to pay for medical expenses. While more HSAs mean more profits for HealthEquity — and function as an effective tax shelter for the wealthy — they do little to reduce the costs or improve the quality of health care for working Americans.

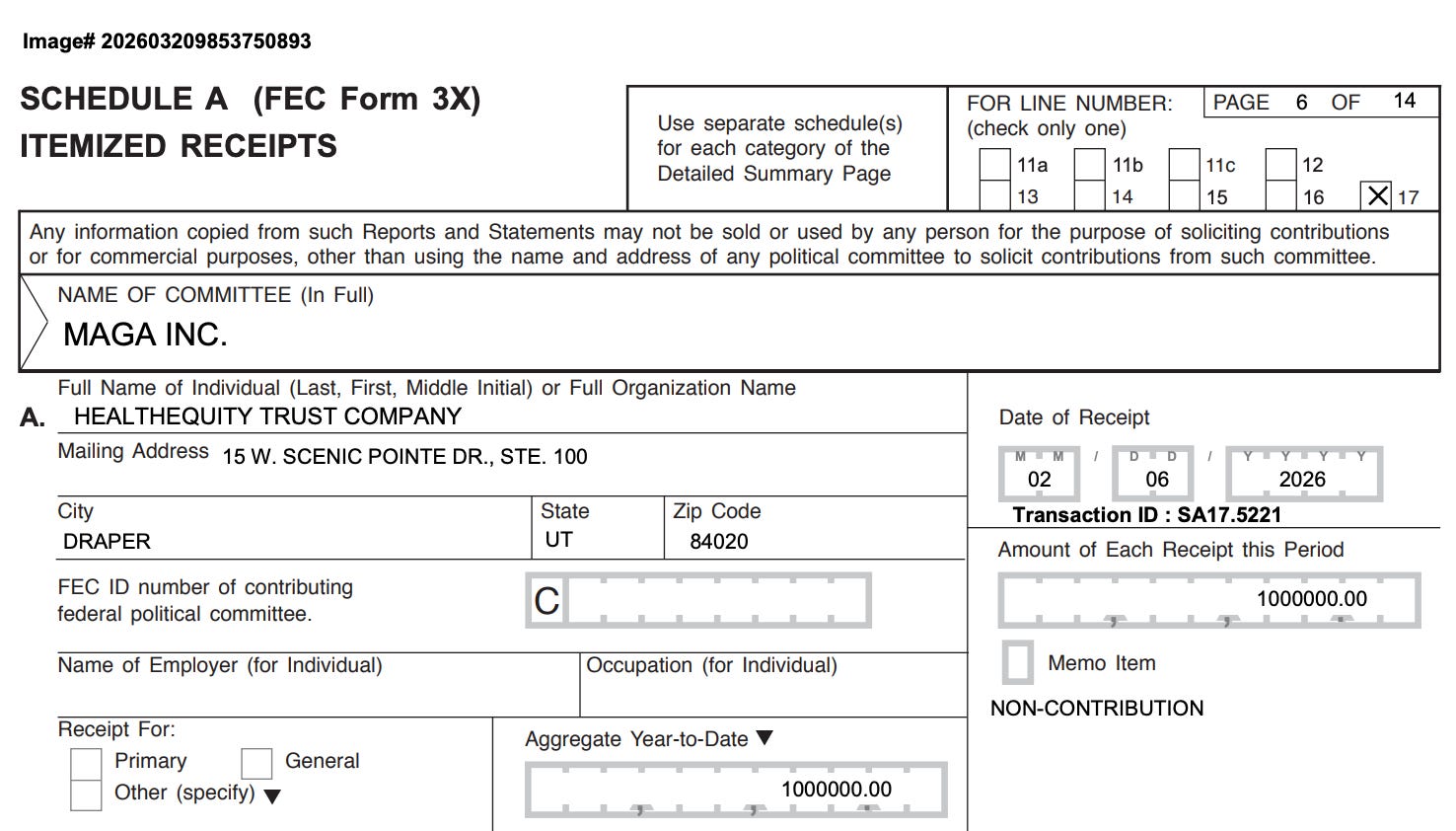

HealthEquity is now making a major push for a more dramatic expansion of the HSA market. Meanwhile, a campaign finance report filed on Friday night revealed that MAGA, Inc, President Trump’s Super PAC, received a $1 million donation from HealthEquity on February 6. The money came directly from the company’s corporate treasury.

Previously, HealthEquity had never made a federal campaign contribution exceeding $5,000.

How HSAs benefit the wealthy and exploit working Americans

Most Americans with access to HSAs cannot afford to fund them. About 40% of Americans have outstanding medical or dental debt. This group, along with many others without current medical debt, does not have disposable cash to fund an HSA. That is why half of all HSAs have balances of less than $500, and one in five have a balance of zero.

Seventy-seven percent of the value of HSAs goes to households with incomes of $100,000 or more. They are also laden with junk fees imposed by HealthEquity and other administrators, which further diminish their utility for people with small balances. The accounts are typically attached to high-deductible health insurance plans that can make necessary care unaffordable.

In a February 24 advertorial published in the Washington Times, HealthEquity CEO Scott Cutler spun the fact that HSAs cause Americans to skip medical care as a positive feature that reduced costs. Cutler said that HSAs give Americans “skin in the game” and prevent “unnecessary utilization.”

Wealthy Americans, however, are able to benefit substantially from HSAs. Since they pay a higher marginal tax rate, they benefit more from each dollar deposited in the account. A couple with $800,000 in annual income saves 37 cents for every dollar contributed to an HSA, more than three times the savings for a couple with $30,000 in annual income.

The real value of HSAs for the wealthy lies in using them as a stealth retirement fund. They can contribute money to the account tax-free. Then invest those funds in stocks and have it grow tax-free. Wealthy HSA holders pay medical bills out of pocket, save the receipts, and reimburse themselves tax-free years or decades later while the money compounds. Even without significant medical expenses, withdrawals after age 65 are taxed as ordinary income, with no minimum distribution required.

Financial advisors recommend that the wealthy pursue this strategy. Thayer Partners, a firm that caters to high-net-worth individuals (HNWIs), published an article earlier this month titled “Health Savings Account: The Ultimate Retirement Health Vehicle For HNWI.” The firm calls HSAs “a powerful wealth-building mechanism that savvy HNWIs are exploiting to maximum effect.”

This tax loophole for the wealthy diverts funds that could otherwise be used to help people who lack affordable health insurance. Over the next 10 years, HSAs will cost about $190 billion. That would have been enough to extend the premium subsidies that expired at the end of 2025 — and are substantially increasing costs for millions of Americans — for at least 6 years.

What the HSA industry wants

The administrators of the HSAs benefit from the creation of new accounts, through fees, whether or not the HSAs benefit the account holders.

The One Big Beautiful bill expanded the market for HSAs by allowing them to be attached to so-called bronze and catastrophic plans available in the ACA exchanges. These are high-deductible plans that previously could not offer HSAs. This change made about 10 million more Americans eligible for HSAs. This population is among the least likely to benefit from HSAs. More than 80% of marketplace enrolees had household incomes of $47,000 or less, making it unlikely that they have significant excess cash to fund an HSA.

In December, the Trump administration’s IRS went even further than the text of the law, expanding HSA eligibility to high-deductible plans offered outside the ACA exchanges.

HealthEquity is not satisfied and is pushing for much larger changes.

In his February advertorial, Cutler advocates allowing HSAs to be offered with any kind of insurance, expanding the market to every covered American. This would include wealthy Americans with generous health care plans and low deductibles. It runs counter to the original purpose of HSAs, which is to help people in high-deductible plans cover out-of-pocket expenses. While it would do little to make health care more affordable, it would allow many more HNWI to use HSAs as a tax shelter. While it’s unclear how many Americans would open HSAs under this scenario, it would undoubtedly cost tens of billions of dollars annually.

Cutler also wants to allow Americans to use HSAs to pay not just out-of-pocket expenses but also health care premiums. This would transform HSAs from a limited vehicle for out-of-pocket expenses to a broad tax subsidy for all health care costs, incentivizing most Americans to open an account. It would quickly become one of the federal government’s largest tax expenditures. Along the way, HSAs would collect fees and interest.

Finally, Cutler calls for increasing contribution limits “to reflect real healthcare inflation.” Annual limits are already indexed to inflation, and the annual limits for a family have increased by $1,000, to $8,750, over the last three years. This is a change that would only benefit the wealthiest Americans because most people who have HSAs do not contribute anywhere close to the annual limit.

HealthEquity began pushing these radical proposals just 18 days after donating $1 million to MAGA Inc.

This is the clearest explanation of yet another gift to the wealth class that I have read. This is by far the most informative use of this platform.

Thank you Judd.

Of course this company has a stupidly inaccurate name like HealthEquity. There's nothing equitable about its proposed reforms.